Strategy & Portfolio

Chimera Investment Corporation (NYSE: CIM) is an internally managed Real Estate Investment Trust (REIT), founded in 2007 and headquartered in New York City. Our business objective is to provide attractive risk-adjusted returns to our shareholders over the long-term, predominantly through dividends and preservation of capital. We have $2.6 billion in total capital consisting of both common and preferred stock. Since inception, we have declared $6 billion common and preferred stock dividends.

Investment Strategy

We seek to maintain a diversified investment portfolio focusing on investing in residential mortgage loans, Non-Agency and Agency residential mortgage backed securities (RMBS) and Agency commercial mortgage backed securities (CMBS).

Our income is generated primarily by the difference, or net spread, between the income we earn on our assets and our financing and hedging costs. We are commonly referred to as a hybrid mortgage REIT because we invest in both non-Agency and Agency mortgage assets. This model provides flexibility in portfolio asset allocation and liability management.

Our Portfolio

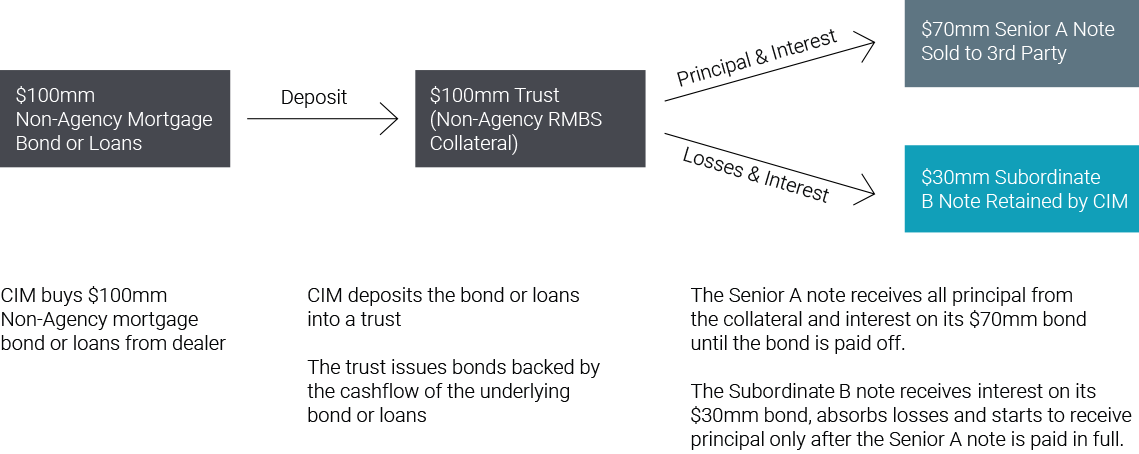

Residential Mortgage Loans: A significant part of our business and growth strategy is to engage in securitization transactions to finance the acquisition of residential mortgage loans. In those securitizations we retain the subordinate RMBS, which typically receive interest income but no principal until the securities senior to them are paid off. This helps mitigate reinvestment risk as principal may not be received for several years after the loan collateral is securitized.

Non-Agency RMBS: We invest in both investment grade and non-investment grade Non-Agency RMBS issued by third parties. We believe this portfolio will provide high risk-adjusted returns over the long-term.

Agency RMBS: We invest in RMBS issued or guaranteed by Ginnie Mae, Fannie Mae or Freddie Mac (Agency RMBS). These securities provide dual portfolio functions by providing both spread income and a source of liquidity for the company.

Agency CMBS: The Agency CMBS we acquire are primarily Ginnie Mae Construction Loan and Ginnie Mae Permanent Loan Certificates. These assets typically have prepayment protection. The borrowers on the underlying mortgage loan generally are required to pay a prepayment penalty if they prepay during the first 10-years of the loan. This prepayment protection generally makes these assets longer duration and thus easier to hedge interest rate risk compared to Agency RMBS.

Funding Strategy

We borrow money, or use leverage, to finance the acquisition of mortgage assets and enhance potential returns on our investment portfolio. We use several funding sources to finance our investments including asset securitization, repurchase agreements (repo), warehouse lines, convertible debt and equity capital.

A key element to our funding strategy is securitization which provides long-term stable financing and structural leverage to potentially enhance returns and mitigate risk. In our securitizations, we generally create senior and subordinate notes. The senior bonds are sold to a third party and we retain the subordinate bonds which include the first-loss bonds that are usually subject to the risk retention rules. In most securitizations, we retain a call option, which, depending on market conditions, we may exercise to liquidate the original securitization trust, receive the remaining collateral and securitize the remaining collateral in a new securitization to reduce the related financing costs or to increase the structural leverage.

Example Securitization*

*A significant portion of the RMBS we acquire through securitization is subject to the U.S. credit risk retention rules which materially limit our ability to sell or hedge such investments as needed, which may require us to hold investments that we may otherwise desire to sell during times of severe market disruption in the mortgage, housing or related sectors, such as those being experienced now as a result of the COVID-19 pandemic.

Consolidated Loan Securitizations